PSA and sustainability reporting are vital for promoting responsible governance, fostering transparency, and ensuring that public entities contribute positively to society and the environment. Moreover, accounting and reporting of contingent liabilities, including the Public-Private Partnership contracts, also contribute to increasing fiscal transparency and stability.

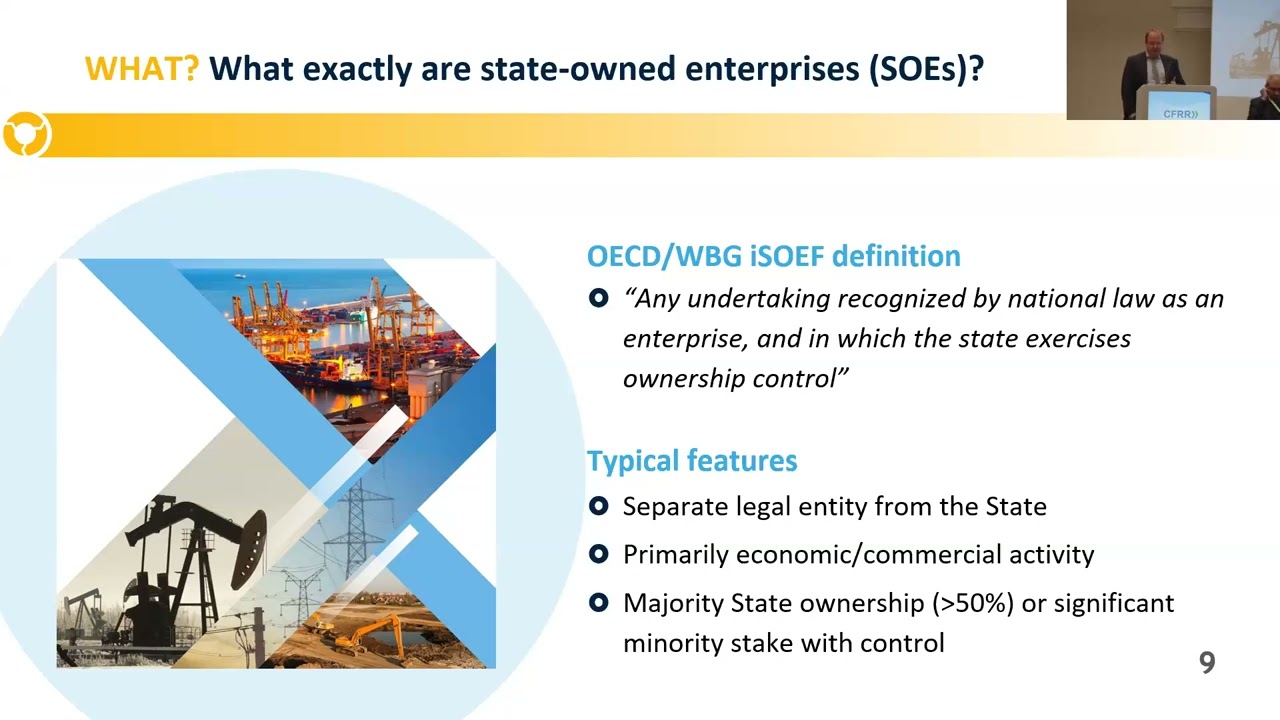

In turn, the State-owned enterprises (SOEs) play a vital role in the economy and society, given their relevance for provision of essential public services, infrastructure development, and job creation. Accounting for SOEs could be particularly complex, considering their unique structure, dual objectives: public and commercial, and relationship with governments and markets.

On the other hand, the role of sustainability reporting in both private and public sectors is increasing, as it incorporates environmental, social, and governance aspects into accounting.

In response to this fast-growing demand, the International Public Sector Accounting Board (IPSASB) just published the first sustainability reporting standard (SRS) for public sector. In this context, the government officials need to become aware and start getting ready for implementation of sustainability reporting practices in their respective countries.

The main objectives of this face-to-face workshop focused on:

- Discussing the latest developments in sustainability reporting and its implications for public sector.

- Discussing the good international practices in terms of accounting for State Owned Enterprises (SOEs), Provisions and Contingent Liabilities (IPSAS 19), and Public-Private Partnership (PPPs) (IPSAS 32).

- Sharing good international practices and exchange experience on the proposed topics.

PULSAR joint Education and Financial Reporting Communities of Practice 10th Workshop - Day 1

PULSAR joint Education and Financial Reporting Communities of Practice 10th Workshop - Day 2